Working on your down payment money to buy a home? Here’s something you need to know…your paycheck can work against your down payment savings plan.

Buying a home requires precision planning, good income, good credit, manageable liabilities and a healthy down payment. As much as 3.5% of the purchase price can be a big factor for many families looking to get their piece of the American Dream. In some areas you will need up to $20,000 to purchase a house. That figure gives you buying ability into bigger dollar amounts and can even be a portion of the closing costs to purchase a house.

Not all money you save is created equal and here’s why. When you save money from your paycheck (as you should for a good general personal financial planning) that money is not automatically eligible to purchase a house. It’s called income for assets. Income for assets in the world of mortgage lending is frowned upon.

For example let’s say you receive your paycheck and your net earnings is $5k. That $5k must be in your bank account for a period of 60 days in order for that money to be considered seasoned. The bank wants to see you had the ability to save the money on your own volition rather than depositing your income for cash to close. If you are currently ‘in contract” to buy a home, these monies if needed, could delay your closing date. If you are “not in contract” plan on these monies being in your account for 60 days if you intend to use those funds.

Using income for a down payment may might not seem like a big deal in the grand scheme of things with all the other components that go into buying a home, however it will be looked closely by bank’s underwriter. Your cash to close can very easily go up bank’s radar fast if you’re using every last hour you can to get your foot in the door.

Following are other monies that can be used in lieu of your paycheck funds:

- Stocks

- Bonds

- IRA

- 401K

- Gift

If cash is your obstacle for buying a home, you have options. It may mean waiting to put an offer in on that house until you have enough money in your bank account or writing a longer contract. Remember every seller has different motivations and timelines for selling. In competitive markets such as Sonoma County every contract is written for 30 days just to get an offer accepted. You will need to plan accordingly with your lender in such situations to have the funds accessible to go, then write the contract aggressively to make your home buying plan a 30 day reality.

Looking to buy a home? Get pre-approved today!

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Mortgage Waiting Periods After Bankruptcy, Foreclosure, Short Sale, and Judgments

Many people believe that a foreclosure, bankruptcy, short sale, or judgment means they will never…

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

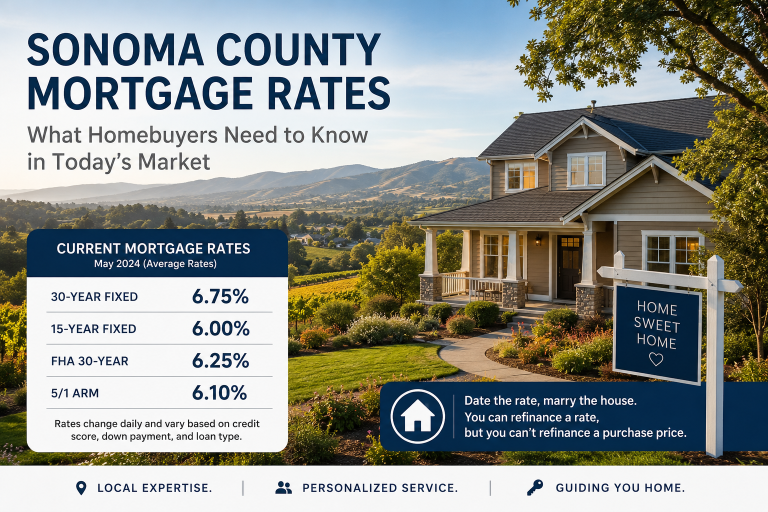

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!