Becoming a partner at your firm is often one of the biggest milestones in a professional career. Whether you’re an attorney joining a law firm partnership, a CPA becoming a partner in an accounting firm, or a physician receiving partnership status in a medical practice, the promotion usually comes with increased income and greater opportunity.…

Finding out you owe money to the IRS can be stressful. Between tax notices, payment plans, and trying to get your finances back on track, many people assume buying a home is no longer an option. Fortunately, that’s often not the case. One of the most common misconceptions in mortgage lending is that owing back…

One of the most common questions we hear from homebuyers has nothing to do with interest rates, credit scores, or down payments. Instead, it sounds something like this: “If my parents or grandparents help me buy a house, am I going to have to pay gift taxes?” The good news is that, in almost every…

If you’re using a VA loan to purchase a home, you may hear the term “VA Tidewater” during the appraisal process. While the name sounds unusual, the Tidewater process is actually a valuable protection designed to help veterans avoid appraisal surprises and provide an opportunity to support a home’s value before the appraisal is finalized.…

One of the biggest misconceptions in mortgage lending is that a high income can solve every mortgage qualification challenge. While income is extremely important, it cannot always make up for weaknesses in other areas of your loan application. When it comes to qualifying for a mortgage, there are three major factors lenders evaluate: income, credit…

Many people believe that a foreclosure, bankruptcy, short sale, or judgment means they will never qualify for a mortgage again. Fortunately, that is rarely the case. Life happens. People experience job losses, medical issues, divorces, business failures, and unexpected financial hardships. Mortgage lenders understand this, and most loan programs have established waiting periods that allow…

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first glance, that logic makes perfect sense. Lower interest rates generally mean lower monthly payments. Lower monthly payments often increase purchasing power. More purchasing power should make housing more affordable. However, that is only part of the story. What many buyers…

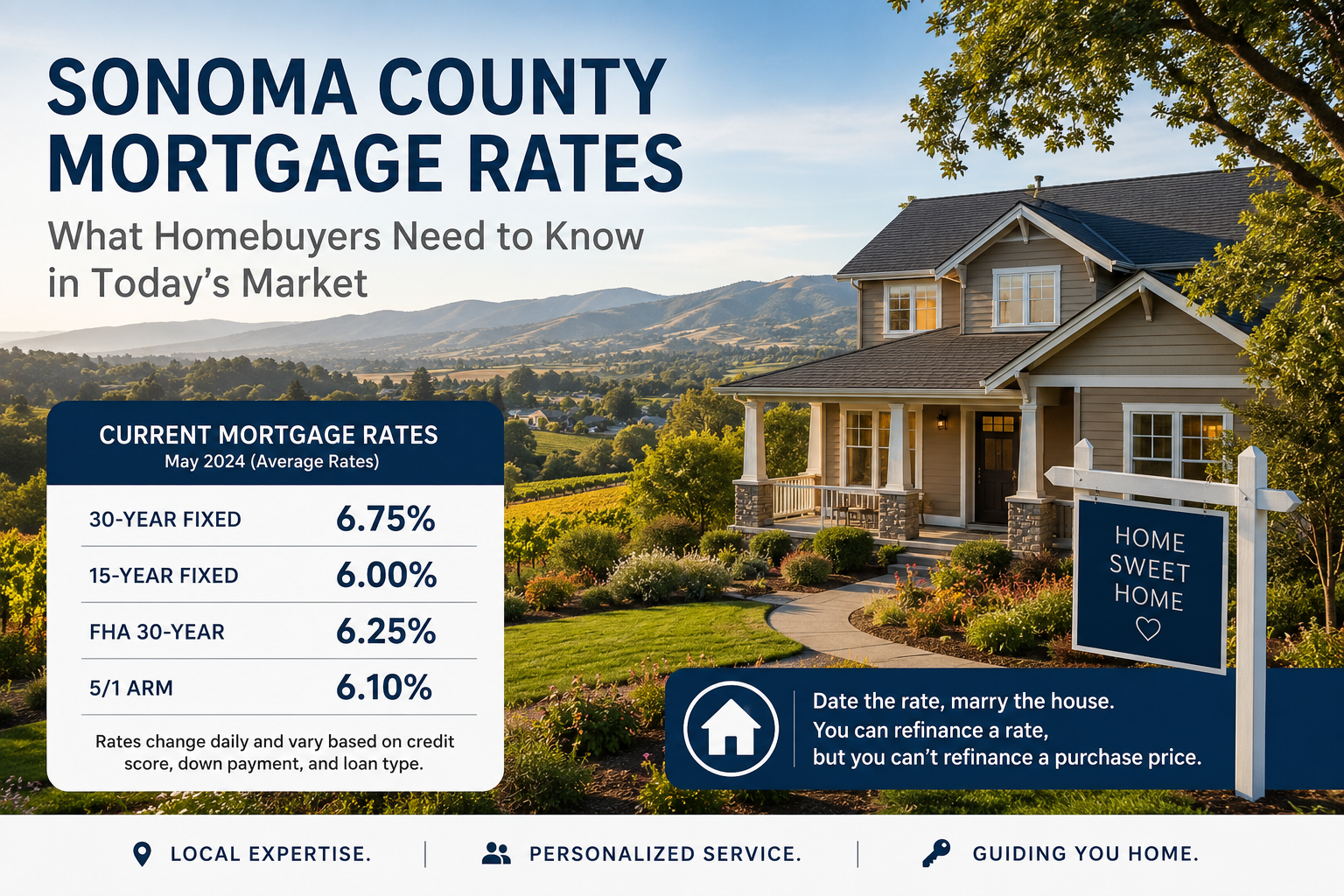

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close attention to mortgage rates. Interest rates have been one of the biggest topics in real estate over the last few years, and many buyers are wondering whether now is the right time to purchase a home or if they should…