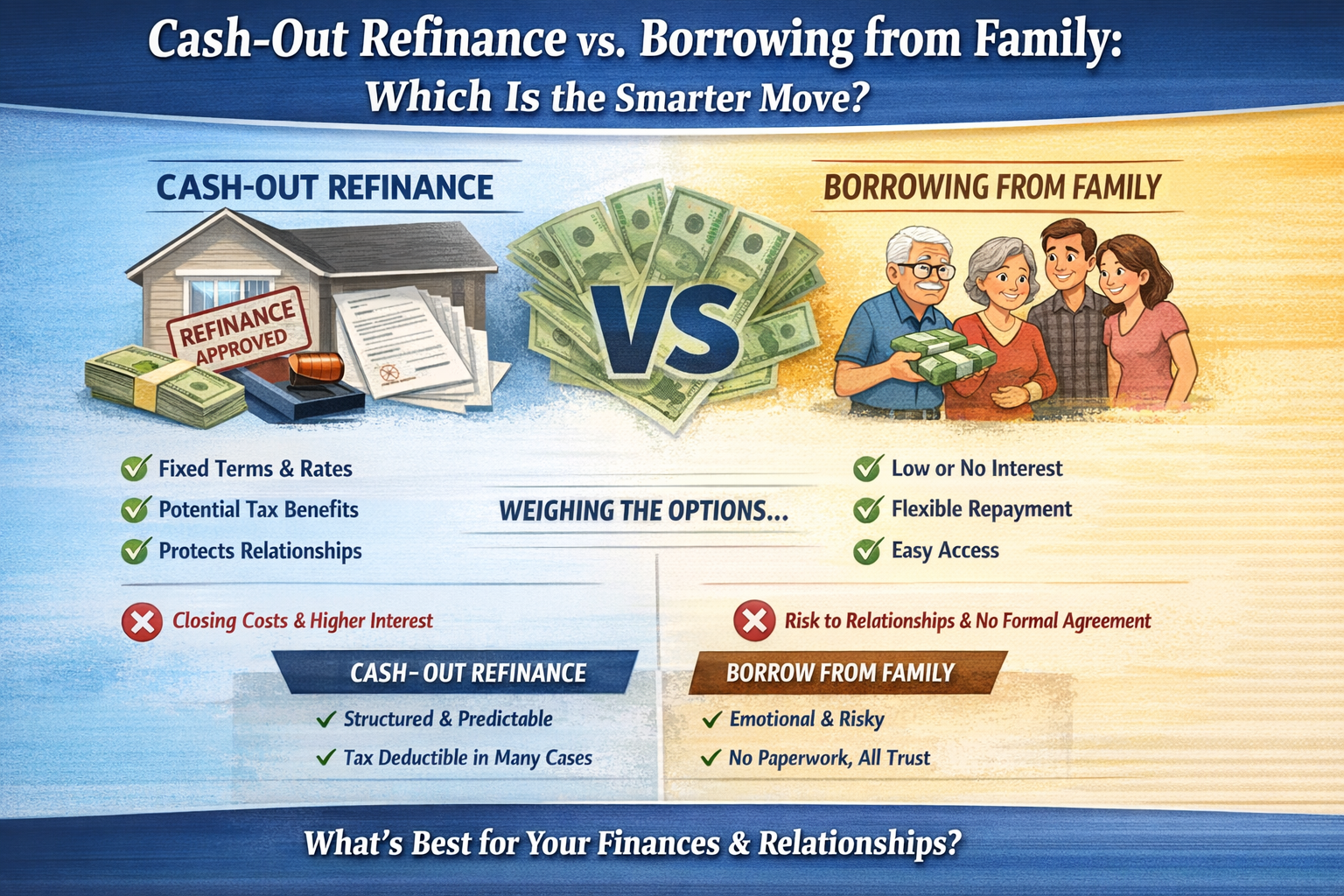

You’ve built equity in your home. Maybe a lot of it. At the same time, you need access to cash—whether that’s to consolidate debt, invest in real estate, fund a business, or handle a life event. Now you’re standing at a fork in the road: Do you tap into your home equity with a cash-out…

Let’s start with a simple but powerful scenario. A homeowner locked in a mortgage at 2.75% during the pandemic. Fast forward to today, and that same homeowner is now looking at interest rates closer to 6.5% on a 30-year fixed. Even if their life has changed—maybe they’ve grown their family or simply need more space—the…

Who you use for a mortgage loan matters. Let’s walk through a very real scenario that happens all the time when someone is considering refinancing their home. Imagine you currently have a 6.25% conventional mortgage. You’re looking at refinancing because you see interest rates drifting lower. You call a lender and they quote you 5.25%.…

Every so often, someone gets pre-approved, looks at homes, runs numbers… and then says, “We’re going to press pause.” That’s okay. But before going on hold, there’s an important question worth asking: What made you want to buy a home in the first place? Because most people don’t wake up randomly and decide to take…

One of the most common objections home buyers provide is this: “I want to wait to get qualified because I need to pay off my credit cards first.” On the surface, that sounds financially responsible. Reduce debt. Strengthen finances. Then purchase a home. But there is a critical distinction that often gets overlooked: Is paying…

For many buyers, the idea of buying a vacant parcel of land and building their dream home—or placing a manufactured home on it—sounds both exciting and affordable. On paper, it may even look cheaper than buying a resale property in today’s competitive housing market. But the reality? Building from scratch, especially on raw land, or…

Many homeowners assume that selling a house with an existing mortgage complicates their tax situation—but in most cases, it doesn’t. Whether you’ve owned your home for two years or two decades, if you’ve built equity and are thinking about selling, it’s important to understand how capital gains tax rules work, especially when a mortgage is…

Buying a home isn’t just about having a place to call your own—it’s also one of the smartest long-term financial decisions you can make. Sure, you’ve probably heard that before, but let’s break it down in plain terms. If your lender can’t clearly explain the core financial advantages of owning a home—appreciation, tax deductions, and…