Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home One of the most common questions homebuyers ask is: “Can I keep my current FHA home as a rental and buy another house using a new FHA loan?” At first glance, it sounds reasonable. Maybe your current…

If you are thinking about buying a manufactured home, one of the most important details to understand is the year the home was built. That single factor can dramatically affect your financing options, interest rate, resale value, and even how easy it may be to sell the property later. Many buyers see an older manufactured…

Let’s walk through this in a real, practical way—because the question isn’t just “can you buy?” It’s “can you buy comfortably?” In Sonoma County, that answer depends on three key things: Home pricesInterest ratesYour debt and lifestyle Right now, the market is more balanced than it’s been in years. Homes are sitting longer, and buyers…

Picture this. You’re in contract on a home. The seller agrees to give you $15,000 in concessions. Now comes the real decision: Do you use that money to: Cover your closing costs? Buy down your interest rate? Or reduce the purchase price? All three options sound good. But they impact your finances very differently—both now…

Buying a home with less-than-perfect credit is still possible—but there are some important rules that can change the entire game if your credit score falls below a certain level. When people talk about FHA loans, you’ll often hear that you only need 3.5% down. That’s true—but only if your credit score is 580 or higher.…

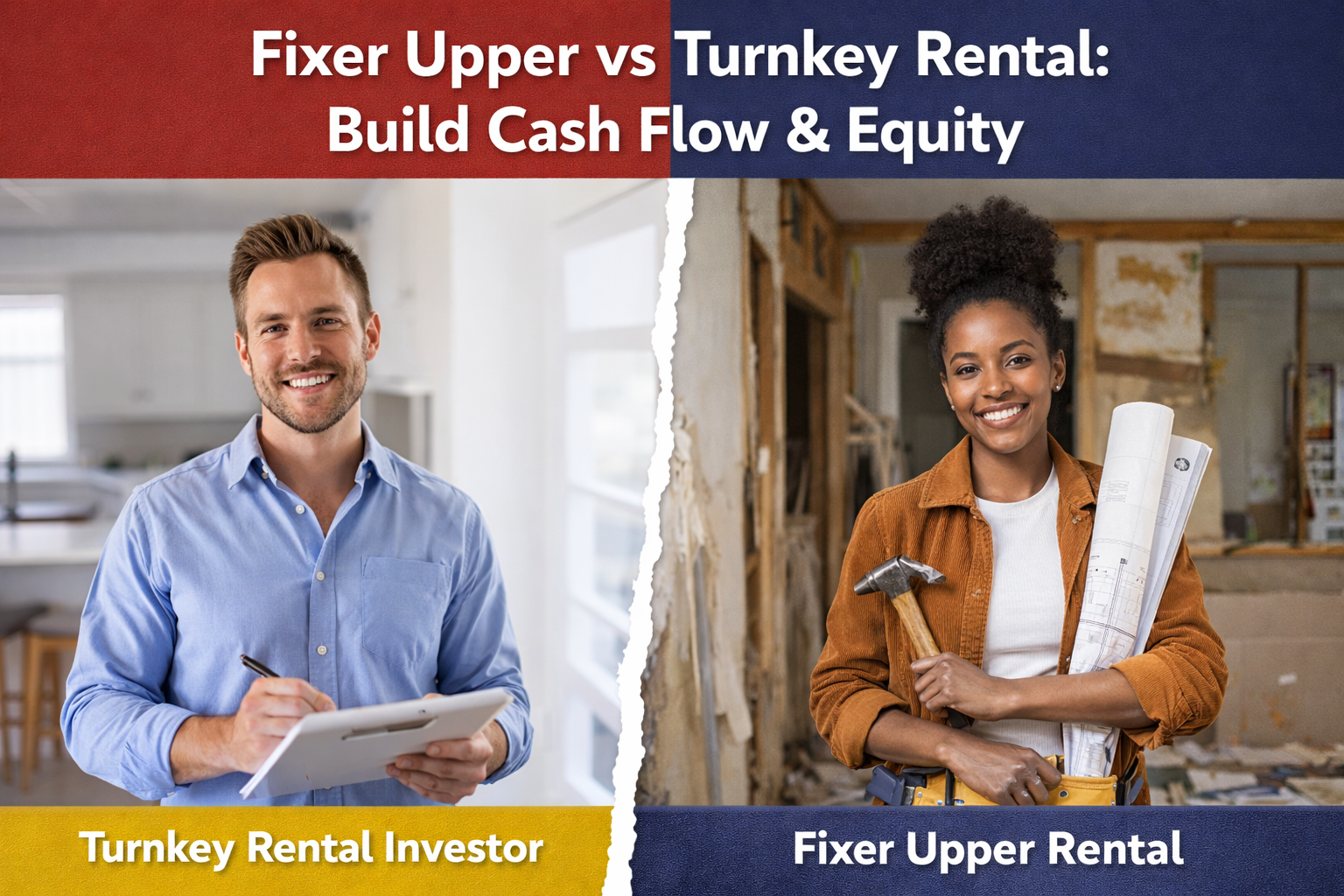

Fixer Upper vs Turnkey Rental: How to Build Cash Flow and Equity (Part 2) In the first part, we talked about how tenants think and why a home doesn’t need to be perfect to be a strong rental. Now let’s take it a step further. This is where the real strategy comes in—how price, repairs,…

Let’s start with a simple scenario. You’re looking at two homes. One is fully updated, clean, and ready to go—but it comes with a higher price and higher monthly payment. The other needs some work—maybe paint, flooring, or a few updates—but it’s priced lower. Which one is the better investment? From experience as a landlord,…

Let’s start with a simple idea: trying to perfectly time the housing market is not a winning strategy. It sounds good in theory. Wait for rates to drop. Wait for prices to fall. Wait for the “right moment.” But here’s the reality—no one consistently gets that timing right. Not individual buyers. Not seasoned investors. Not…