Buying a house can always be a daunting consuming feat. Caring consumer obligations such as car loans can further complicate a picture of that otherwise could be more financially lucrative. When you carry on a car debt whether it’s at lease payment or whether it’s a financed payment you’re handcuffing a portion of your future income…

Auto loans help your credit from a credit score standpoint, but they also limit your borrowing power and at the end of the day probably do more harm to your financial picture for qualifying to buy a home than good. It doesn’t matter if your interest rate is 1% or 0%. If your income is not enough to support a housing payment, it might be time to think about getting rid of the car.

Take the following considerations into account:

$10,000 per month of income car payment should be $200 per month

$9,000 per month of income car payment should be $180 per month

$8,000 per month of income car payment should be $160 per month

$7,000 per month of income car payment should be $140 per month

The list goes on as you can see for every $1,000 of income you want your car payment to be $20 per month less. For every $20 per month of car payment you want to have your income be $1,000 upwards in support of that calculation.

Here is why…

Many families don’t have just car loans or car lease payments there’s also credit card payments, personal loan payments to name a few. The other 5 to 10% of your income should be allocated towards those monthly expenses.

Ideally don’t have those monthly expenses and use the other 5 to 10% of your income towards saving. The ability for you to purchase a house should be predicated on your ability to save money beyond your mortgage payment (not just the principal portion of your monthly repayment on your fixed rate mortgage).

This also means any monies you’re contributing to your 401k what you should be doing through your employer anyway if you are a W-2 employee. If you are a self-employed wager contributing to an IRA is a fantastic way to plan for retirement.

The bottom line is when you purchase a house regardless of its a first-time a second time or third time you want your monthly consumer liabilities to be as absolutely low as possible because the lender is concerned about the payments that you are making on those obligations not the interest that you’re paying which is what you focusing on.

To be successful as a home buyer, you need to think like the lender focus on the monthly payment. By whittling down your monthly expenses, you can best position yourself for purchasing a home. This can be accomplished by paying the monthly debt off, possibly getting a cosigner depending on what your future income is or work on changing your role or occupation, so you can earn more money for the purposes of getting out of debt faster while purchasing a home and saving at the same time.

Looking to buy a home? Get a no cost quote now.

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

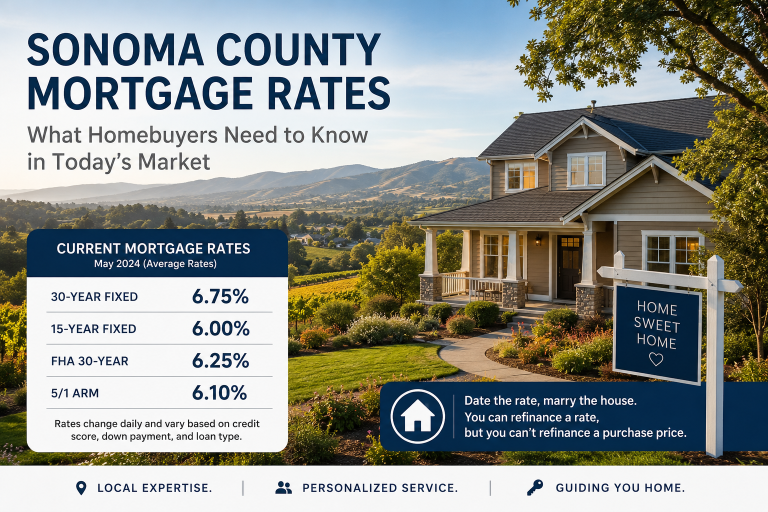

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

What Income Do You Need to Buy a Home in Sonoma County in 2026?

Let’s walk through this in a real, practical way—because the question isn’t just “can you…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!