HUD recently announced the FHA Loan Limits for 2019 have been increased. This increase includes VA loan limits for both refinancing and home buying.

These changes will represent more opportunity for families to finance bigger mortgages going forward as the limits across the country have increased. Even the low-cost areas which represents 65% of the conforming loan limits set at $484,380 have increased up to just over $314k.

For example, in Sonoma County California the loan limit was increased to $704,950. This means you can now purchase a house in Sonoma County California with 3.5% down for a single-family residence and get an insurable 30-year fixed rate mortgage up to $704,950.

This also means you can refinance a first mortgage and a second mortgage as a rate and term refinance doing the first and second combination into one new loan and the loan can still be considered a rate and term refinance. This can be particularly valuable for someone who has a first mortgage and a home equity line of credit that is an adjustable rate that they are now combining into one new loan. FHA loans can be finance up to 96.5% loan to value. Families buying homes that don’t have a big down payment but have strong income and sufficient credit can also now enter the market and be able to play ball at a higher loan amount to help in a competitive purchase offer situation.

Both FHA Loans Limits and VA Loans in community property states require the lender pull the credit of the spouse and their debt is counted against the payment to income ratio for the mortgage. One caveat to this is that the VA will soon be announcing that income from the spouse whose debt is being counted in a community property may be offset with their incomes subsequently not adversely affecting the primary borrower’s borrowing power.

These FHA changes all represent a borrower being eligible for a mortgage after the following negative derogatory credit situations:

- 3 years after a foreclosure

- 3 years after a short sale

- 2 years after a Chapter 7 bankruptcy

- 1 year after a Chapter 13 Bankruptcy

One thing however about the FHA that holds does is that you are unable to refinance an FHA loan for a borrower into a new FHA loan who has not owned and lived property and lives in the property for the most recent last 12 months. If you’re looking for an FHA Loan or need some mortgage guidance reach out today for a complimentary cost quote.

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

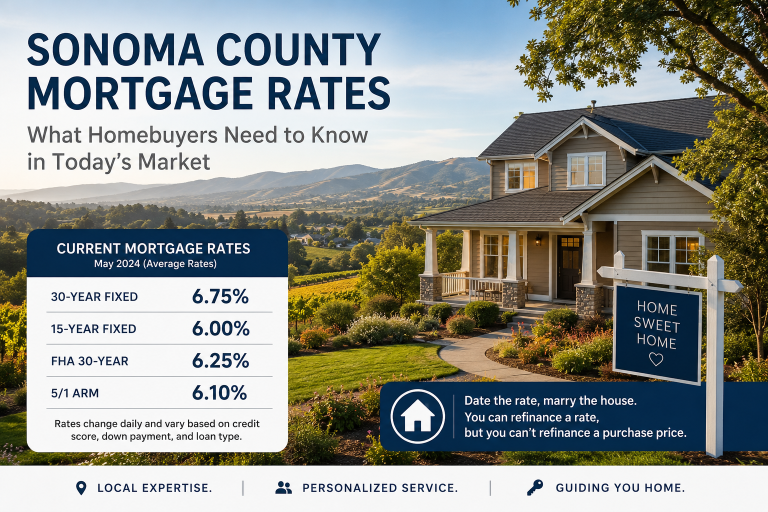

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

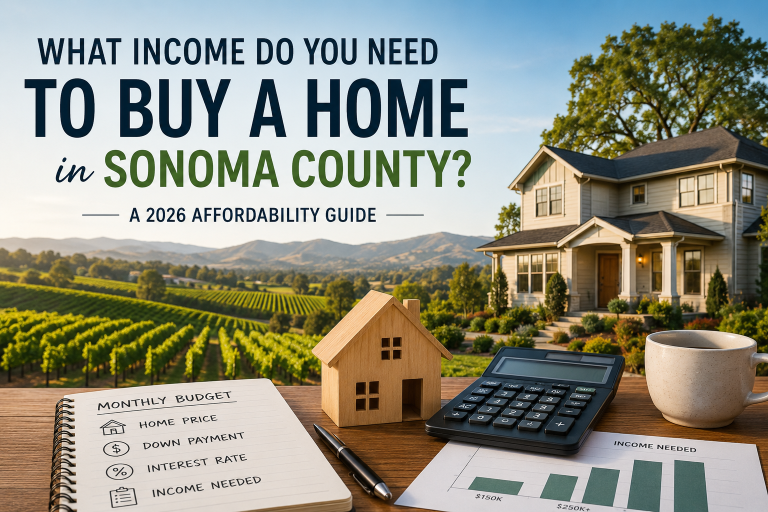

What Income Do You Need to Buy a Home in Sonoma County in 2026?

Let’s walk through this in a real, practical way—because the question isn’t just “can you…

Seller Credit vs Price Reduction vs Rate Buydown: What Saves You More When Buying a Home?

Picture this. You’re in contract on a home. The seller agrees to give you $15,000…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!