Consumers looking into the possibility of buying a home should know you need less money than you think. Here’s the amount of cash you need to buy a home, and what you need to know using as little down as possible…

Cash Needed

Contrary to popular belief, you don’t need 20% down. The minimum down payment you need to buy a home on the broader picture is 3.5% down with an FHA Loan, on a 30 year fixed rate mortgage. This 3.5% down payment is a factor of the home price on a loan size up to the high balance FHA County Loan Limit. For example in Sonoma County, California, means up to $520,950, and in some higher cost areas, such as Marin County or San Francisco County, that number goes up to $625,500 for a single-family residence.

Alternatively, on a Conventional Loan you need only a 5% down payment up to $417,000 loan size. Should your loan size exceed $417,000, another 5% down payment kicks in, for a total of 10% down needed all the way to the maximum County Conforming Loan Limit

What To Know When Buying A Home With Little Down

- Your mortgage payment will be higher than with more down- these are the three drivers that inflate the payment ….interest rate, larger loan size, as well as possible PMI.

- You should have manageable monthly debts. The monthly debts including credit cards, car loans, and any form of payment obligations should be manageable in relationship to your income. Your income will need to be relatively high to include the proposed mortgage payment for the purchase price you are seeking as well as being able to cover these other liabilities.

The percentages when buying a home are important to know, but it is significantly easier to work with the monies you have or have access to, than to get wrapped around the axle about down payment percentages. Make no mistake the mortgage company can work this factorization out for you very easily or you can do it yourself. You can take the amount of money you have and divide that number by the purchase prices in your area to determine the exact dollar percentage.

For example let’s say you have $30,000 to spend on buying a home and you know that housing prices in your area are $450,000 that means you have a 6.7% down payment, enough for an FHA Loan. If your loan professional asks you how much money you have to spend on buying a home in terms of your own funds and possible gift funds the answer should be some sort of dollar amount, not “Well how much do I need?” The reason is this. How much you’ll need to buy a home is going to be predicated on the purchase price of the property and is a continual variable until you get into contract. Start with the monies you have. Assuming you have $30,000 to spend on our $450k home example, closing costs on a $450,000 home will easily equate to $10,000, so of the $30,000, $10,000 would come right off the top for closing costs leaving you with $20,000 as a down payment still meeting the cash to close requirements on an FHA loan.

Other No Money Down Options Including The Following:

- VA- program allows for no money down, 100% financing for US military veterans only

- USDA- program also allows for no money down, 100% financing as long as you are purchasing a home in a rural area and you meet USDA’s annual low income thresholds

Alternatively, gift monies can be used to purchase a home with as well. Typically lenders like gift monies to come from some sort of a blood relative, but this is not a broad guideline do check with your individual lender on a specific basis. Additional funds that can be used for the acquisition of a home are:

- stocks, bonds, IRA and 401(k), monies can be pulled from these accounts to purchase a home usually with special provisions

- gift money as long as it can be documented in some form of a bank account can also be used along with providing an executed gift letter

- selling of personal property such as the sale a boat or a motorcycle for example can be used for a down payment and/or closing costs- documented with a bill of sale and paper trailing of the funds

- security deposit refund on current rental obligation this can also be used, but needs to be planned for on the front end so as to properly communicate time frame expectations with your landlord

- Tax return refund

- cash can be used as long as the funds have been seasoned in some form of a bank account for the last 60 days

If want to buy a home or want to get on the path of doing so in the future here are some steps to consider to help meet this goal….

- Identify what monies you have in the bank now, and from what sources.

- Next, get “read” on what housing prices are like in your area via online research or connecting with a good local real estate agent

- Take the amount of cash you have and divide that figure by an estimated sales price range in your area so you can get a feel for how much cash you will need to purchase XYZ home. Closing costs become another crucial factor, but the main goal is determining if you have enough cash to play with. Based upon these action steps, talking with a mortgage lender about getting qualified or how much money you’ll need to save in the longer term picture would be a prudent step in making your home purchase ultimately successful.

Thinking about buying a home? Begin by getting a complementary mortgage rate quote online today !

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

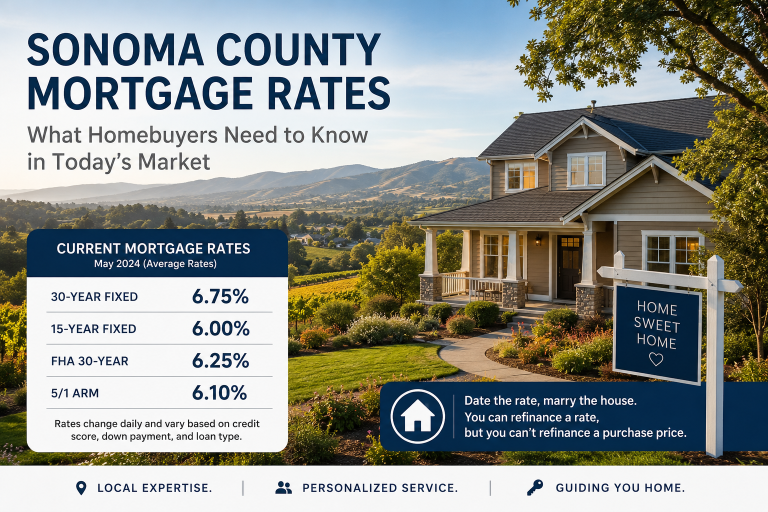

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

What Income Do You Need to Buy a Home in Sonoma County in 2026?

Let’s walk through this in a real, practical way—because the question isn’t just “can you…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!