If you have the need to borrow money, but you don’t want to tap your assets cash out refinancing your home could be a good move. Here’s what to consider when determining what option for cash out refinance your home makes the most financial sense…

Generally, when expense such as needing a new roof, or redoing your backyard presents itself cashing out refinancing might make sense. When you cash finance an expense you forego the future benefits of that money working for you and compounding overtime. The other option of course is to finance the expense. There’s two ways most borrowers use to accomplish cash out refinancing.

Home-equity lines of credit–are a good low cost option to access your home equity. Most are a few hundred dollars at best obtain, don’t require a full appraisal report, and offer the flexibility of being able to access funds easily. The home-equity line of credit is an adjustable rate loan tied to the prime rate. Typically, rates on such loans are under 4.5% with excellent credit. Know this-about home-equity lines of credit are adjustable rate loans.

Looking at the economy with the Federal Reserve poised to tighten interest rates in the future it is reasonable to assume having a higher payment and a rate over time. In short a home-equity line of credit will allow you to access your home equity, but generally should be paid off in full in 1-2 years. If you don’t have the capacity financially to pay off the loan in full looking at a fixed rate new first mortgage might be a more advantageous route with greater predictability.

New first mortgage

Fees can range in the $3k area depending on your desired loan size. Typically, most banks will let you cash out refinance up to 75% loan to value with varying credit scores. In other words the credit capacity for cash out refinancing your home is more flexible if there is credit issues or qualifying issues that otherwise home-equity line of credit thanks could be very sticky about. Refinancing on a 30 year fixed does mean you’re paying the interest expenses over a 360 month period of time. A sound bet wold be to make principal prepayments if you have the financial. Making extra prepayments even as simple a 13th payment once per year can have a dramatic affect on your pay time frame and interest expense. The cost of predictability is the fixed rate loan for your cash out refinance. While a 30 year fixed rate mortgage costs more, it also means the payment remains unchanged over time.

If you are undecided talk to a lender. A good one can walk through the pros and cons of each options arming you with the information necessary so you can make the most informed choice with your finances.

Looking to get a mortgage? Start now with a free quote.

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Mortgage Waiting Periods After Bankruptcy, Foreclosure, Short Sale, and Judgments

Many people believe that a foreclosure, bankruptcy, short sale, or judgment means they will never…

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

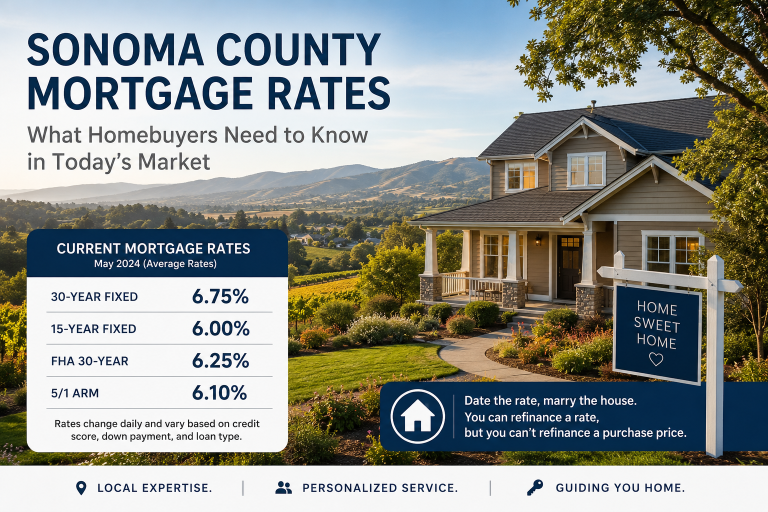

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

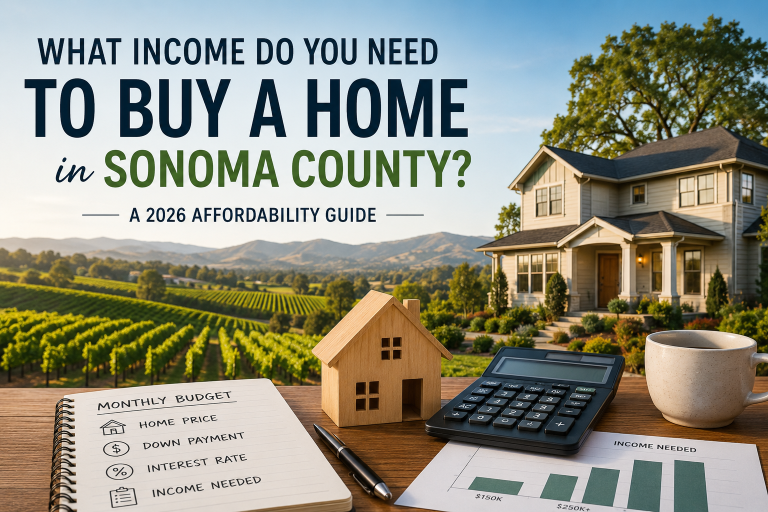

What Income Do You Need to Buy a Home in Sonoma County in 2026?

Let’s walk through this in a real, practical way—because the question isn’t just “can you…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!