Over the past week, there has been a lot of noise around mortgage rates. Headlines moved fast, social media lit up, and many buyers and homeowners were left wondering the same thing: “Are rates finally coming down?” The short answer, as of mid-January, is no. Mortgage rates are essentially unchanged. Last week, President Trump made…

Owning a valuable home feels great—until your checking account says otherwise. Many homeowners are house-rich and cash-poor: sitting on significant home equity but struggling with day-to-day expenses. On paper, they look financially strong. In practice, they’re stretched thin. The key to long-term stability is finding balance—protecting equity while keeping your cash flow flexible and healthy.…

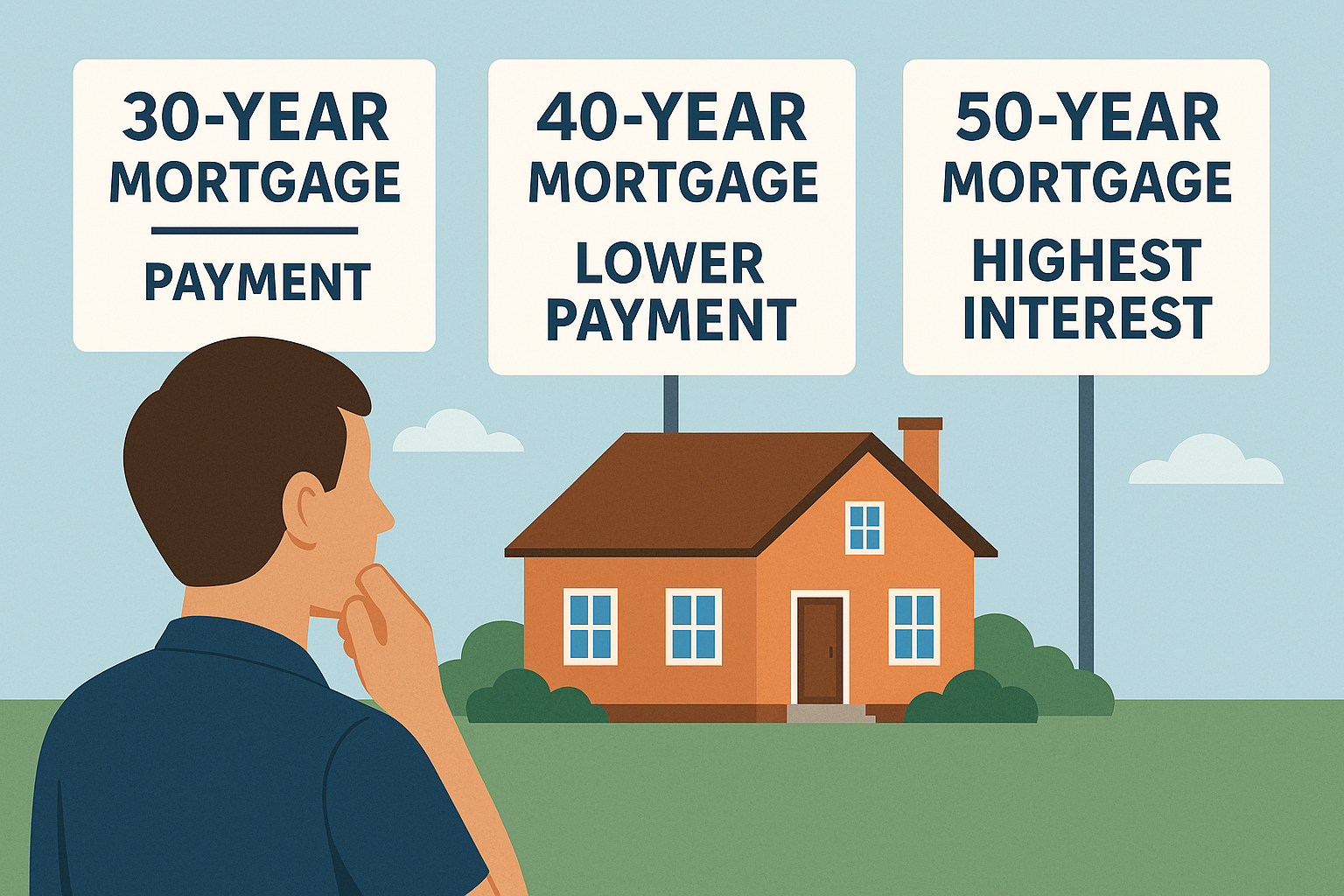

When you stretch a mortgage term out to fifty years, it changes the entire financial picture of buying a home. Yes, the payment drops. Yes, the loan becomes “affordable” on paper. But there’s a real cost hiding underneath that lower monthly payment—the amount of interest you’ll pay over time balloons, often reaching levels most families…

Buying a home is often described as the ultimate step toward financial independence, but it isn’t always the best move for everyone. In some cases, renting provides more flexibility, better cash flow, and less stress than taking on a mortgage. Knowing when to rent instead of buy can save you money and help you stay…

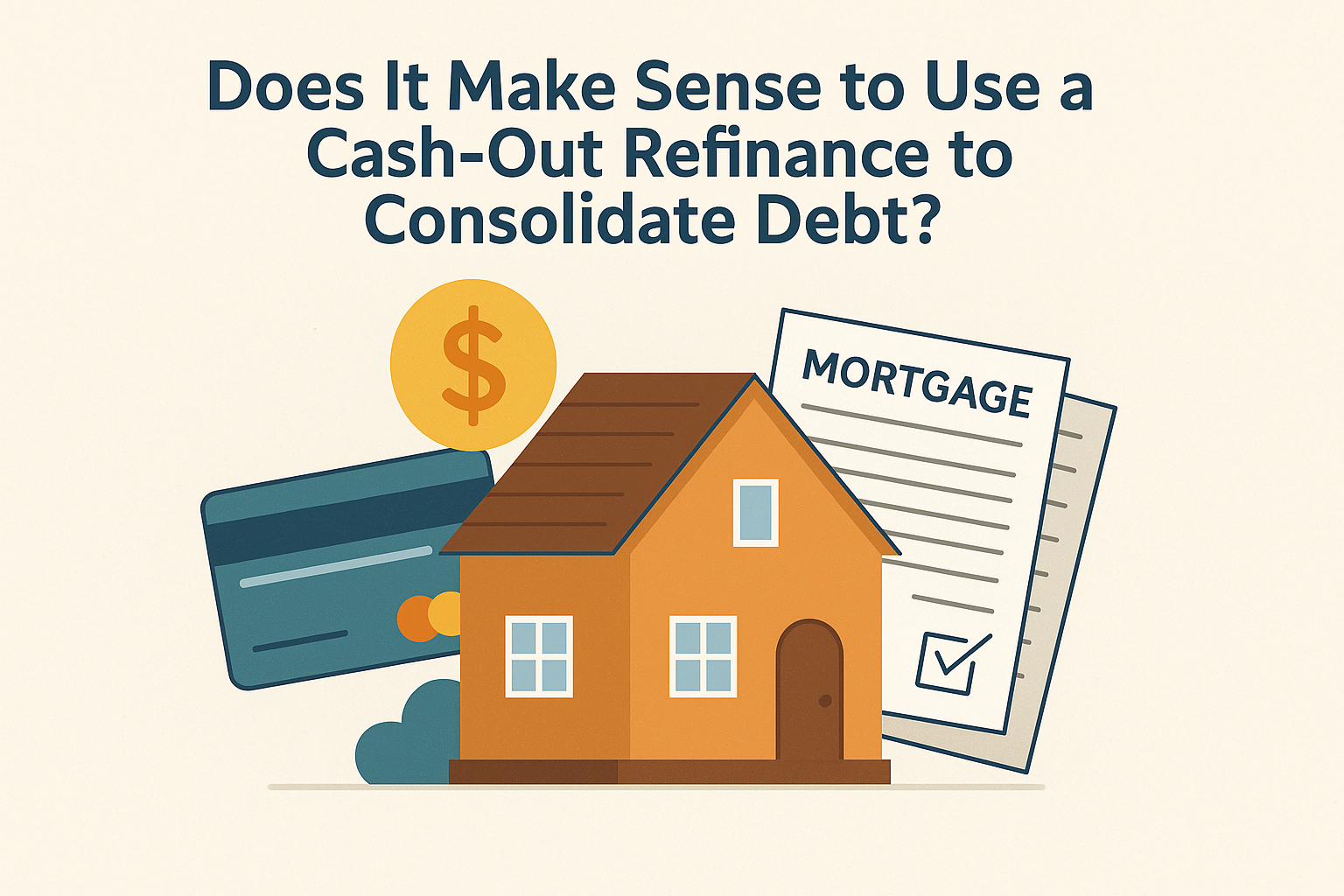

Rising credit card balances and high-interest personal loans can put a strain on your monthly budget. One option many homeowners consider is a cash-out refinance to consolidate debt. This strategy can simplify payments and lower interest costs, but it’s not the right move for everyone. Understanding how cash-out refinancing works and weighing the benefits against…

If you’re receiving Section 8 housing assistance and think that owning a home is out of reach—you’re not alone. Many first-time homebuyers don’t realize that you can actually use your housing voucher as income to qualify for a mortgage. Yes, really. In fact, if you’re receiving consistent Housing Assistance Payments (HAP) and you’re part of…

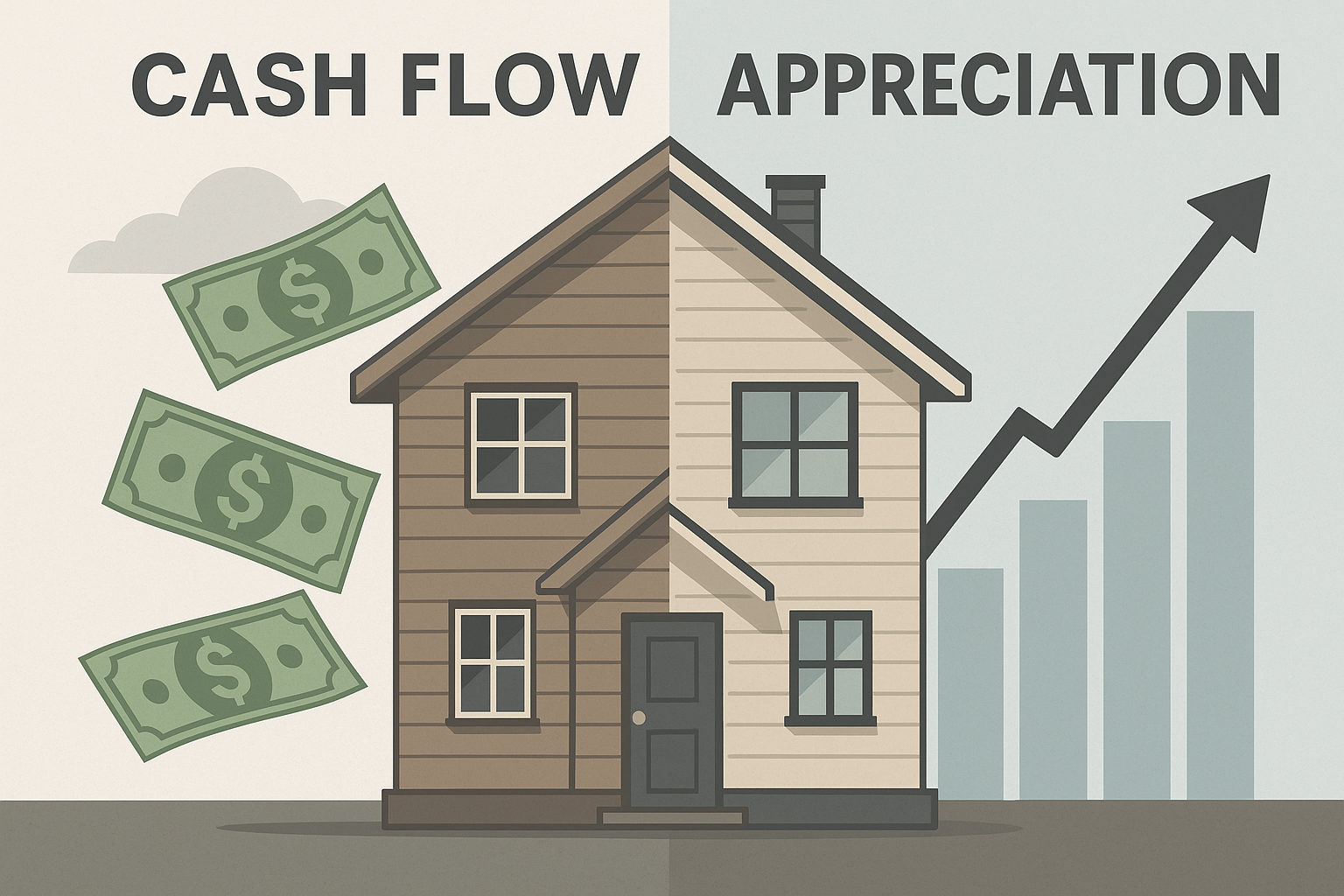

When you invest in real estate, one of the first decisions you face is whether to focus on cash flow—steady monthly income—or appreciation—long-term property value growth. Both can build wealth, but the path you choose should reflect your financial goals, risk tolerance, and local market conditions. Understanding the strengths and trade-offs of each approach can…

On September 17th, 2025, the Federal Reserve cut interest rates—a move that had many people instantly thinking mortgage rates would drop too. But if you’ve been watching this closely, you know it doesn’t work that way. In fact, this exact scenario played out before. Back in June and again in September of 2024, everyone expected…