Here’s a Better Way to Think About It

If the home just hit the market—say it’s been listed for less than 30 days—it’s still considered “fresh.” In that case, offering within 5% of the list price is a good rule of thumb if you want to be taken seriously and still have room to negotiate.

On an $800,000 home, 5% is $40,000. That means a solid starting offer might be somewhere in the $760,000 range, depending on condition, comps, and what else is happening with the listing.

Now, if the home has been sitting for 60+ days with no major activity, that’s when you might have a little more room. You could stretch toward 10% below asking, which puts you around $720,000 on that same $800,000 property. At that point, the seller may be more willing to negotiate.

But once you go past that 10% threshold—like offering $690,000 on an $800,000 listing—you’re running the risk of getting zero response, no counter, and being completely dismissed as a non-serious buyer. And I see that happen a lot more than people realize.

Interest Rates Don’t Guarantee Price Cuts

Another common myth I hear is: “Well, rates are high—sellers have to lower the price, right?”

Not necessarily. Yes, higher interest rates have softened buyer demand in some areas. But inventory is still tight in many markets, and there are plenty of buyers who will stretch for the right property, even if it needs work. Some are investors. Some are future homeowners with a longer time horizon. And some just want to lock in the property now and deal with the upgrades later.

Just because a home isn’t move-in ready doesn’t mean it’s a distressed sale. Sellers still have the option to wait, to relist later, or to accept a better offer that may come in tomorrow.

Be Strategic, Not Emotional

If you’re serious about a property, the best strategy is to come in strong, within 5–10% of asking, and give yourself the chance to get a counteroffer. That opens the door to a conversation—maybe the seller meets you halfway, maybe they offer credits instead of a price cut, or maybe they throw in something else that makes the deal work.

But if you come in too low, you may not even get a seat at the table.

Final Thoughts

There’s nothing wrong with wanting a deal—especially if you’re willing to put in the work. But keep your expectations aligned with the current market and the seller’s position.

Making a smart offer is about more than just the numbers on paper. It’s about understanding timing, market momentum, and how to position yourself as a serious buyer who respects the value of the property—even if it needs a little love.

If you’re not sure how to frame the right offer or want to explore how much room you really have in a deal, let’s talk. I’m happy to walk you through the options, help you run the numbers, and get you into a home that works for your budget and your goals.

Looking to get a loan? Get a free quote today!

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Income, Credit, and Down Payment: How Mortgage Approval Really Works

One of the biggest misconceptions in mortgage lending is that a high income can solve…

Mortgage Waiting Periods After Bankruptcy, Foreclosure, Short Sale, and Judgments

Many people believe that a foreclosure, bankruptcy, short sale, or judgment means they will never…

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

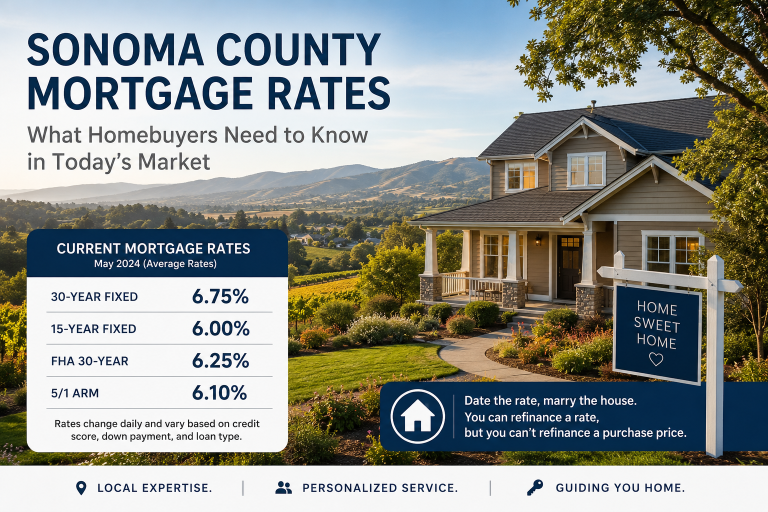

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!