Consumers shopping for a mortgage typically concentrate on attaining lowest possible interest rate. Rates have risen slightly in recent weeks as a more exuberant stock market has taken shape. Current consensus points to more consumers entering the mortgage market, motivated to take action, as a result.

Factors At Work

The financial markets, jobs data, and the Fed continue to support low rates, shifting consumer focus onto interest rate as the catalyst for taking out mortgage financing. As attractive as rates are, ability to qualify for the loan becomes an entirely different picture. Even the most financially savvy folks are falling subject to underwriter’s scrutiny for a flawless credit package.

Concentrate on qualifying

Most consumers would be more suited to concentrate on ability to procure financing aka passing credit standards rather than what their interest rate and payment is going to be. After all what good is the rate and payment if you cannot get the loan in the first place?

The perfect mortgage loan borrower, lenders don’t want you to know:

- one stable W-2’ed job for the last 24 months

- single source of income per consumer

- full supporting income and asset information including all pages all schedules

- no fluctuating income

- transaction is a primary home

- monthly income is three or more times higher than total monthly liabilities including total mortgage payment

- one or no other real estate owned

- same residence history for the last 24 months

- at least 40% equity in the transaction

- middle credit score 760 or higher

- no other cosigners or any other parties on title

- consumer has full access to funds needed to secure financing

- no cash deposits in bank account larger than 25% of the monthly income

- no business losses on the tax return

- six months of mortgage payments or more liquid in the bank with one sole person listed on each account

- no additional businesses listed on the tax return

- low or no monthly liability payments

- use of a payroll company if a business owner

*Don’t meet one or more of these requirements? Not to worry, financing is still attainable, however more attention will be given to determine ability to qualify.

If your credit profile matches the ideal credit profile above then by all means, compare mortgage offers by rate and cost alone. Loan qualifications are mostly standardized, universal from lender to lender across the board, providing a level playing field for all.

What to watch for when trying to qualify for a loan

The first sign is when the mortgage lender continually asks for updated financial documentation or when financial documentation supplied causes more questions. Best example- providing updated bank statements to the lender causes more questions due to additional deposited funds.

Another common sign you’re having a challenge with qualifying is the fact that the lender is taking longer to close the transaction and/or there is an interest rate lock extension which depending from lender to lender, you may or may not be charged for.

Ultimately, due to the tight underwriting constraints set forth by the financial markets, ability to secure financing is crucial and will certainly remain in place moving forward. The consumer looking for a loan today doing their due diligence in comparing mortgage quotes would best serve themselves by getting qualified with a lender first, followed by comparing rate, payment and costs.

Share:

Posted in:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

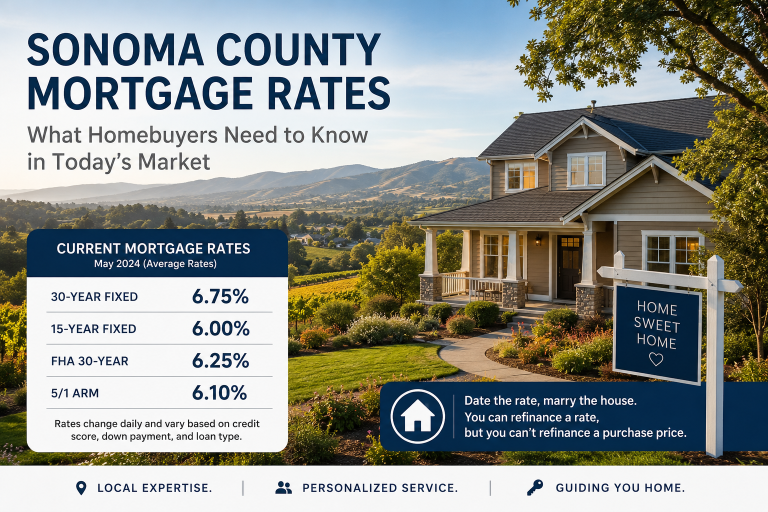

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

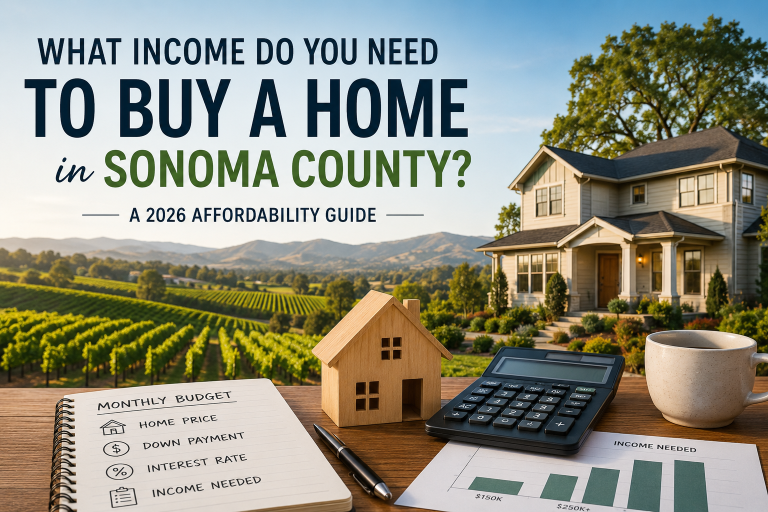

What Income Do You Need to Buy a Home in Sonoma County in 2026?

Let’s walk through this in a real, practical way—because the question isn’t just “can you…

View More from The Mortgage Files:

2 Comments

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!

[…] might find in lender during your comparative loan shopping that is substantially better than the other competitors. Ask yourself the question why? How is he […]

[…] in order for it to be considered a unit in order to use revenue generated from that rent for mortgage qualifying purposes. The additional room in your single-family home, you’re renting out cannot help you […]