Buying home is probably the largest financial transaction you will ever do life. Where you store your down payment funds can mean difference between a smooth or dicey process…

Buying a home does require a down payment of at least 3.5%. While there are programs which require no money down, most have more restrictive income requirements. For the purposes of the broader appeal, a down payment of at least 3.5% is necessary to get your foot in the door plus closing costs. In some markets such as Sonoma County, California you may need as much as $20,000 to buy a home-all dependent on your geographic area.

Problem area 1: Another party’s account

Let’s say for whatever reason you store your money in your parent’s bank account. It’s your money; you earned it, but let’s say mom and dad manage your finances. If you want to use this money, your folks would have to sign a gift letter stating the money is donated. Even though the money is not technically gift funds because it is your money, that’s not how a mortgage company views it. An account that is yours on paper is considered to be your money. An account that contains funds with another party’s name in any way is going to require more paperwork. Best practice to keep the money in a separate savings account that generates little or no activity. One caveat to this- is true donor funds from mom and dad, they will need to provide a gift letter stating those monies are a gift as well as a bank statement to show they have the ability to provide those funds as donors.

Problem area 2: You’re safe

Hiding your money at home in a safe away from the eyes and ears of banks does not help your case either. All financial institutions have strong anti-money laundering laws to prevent criminal activity. The monies you use to buy a home must be in your bank account for a period of 60 days or the monies can be gifted. Cash deposits from “side jobs” you do for friends for example will create conditions (milestones that must be met) from your mortgage company within your loan process. Do yourself a favor. If you serious about buying a home use a bank account and play the rules banks follow.

Problem area 3: Your primary checking account

Checking accounts can be problematic for home buying. If your cash to close on the house is in a separate checking account you use to save money, then you should be ok so long as you are not spending from this account. If you are obtaining gift money or moving any money from a savings account directly into your primary checking account and then from your checking account into escrow on your new home purchase, you could have problems. When you put money into your checking account that you run your normal monthly ledger off of, it can appear on paper like you are spending your down payment! If your cash is tight to get your foot in the door anyway, this is something you want to avoid at all costs. Keep your money in a savings account or an asset bearing account away from your primary checking account. A solid best practice when receiving donor funds is to have the donor wire the funds directly to escrow bypassing your bank accounts altogether. Doing so will save you time resulting in a smoother, faster loan process.

If you are trying to buy a home and need guidance, talk to an experienced mortgage professional that can walk you through the many intricacies in today’s world of financing. The process to buy home is always going to be paperwork heavy and what you do with your money can make all the difference.

Looking to buy a home? Begin with a free mortgage rate quote online now.

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Mortgage Waiting Periods After Bankruptcy, Foreclosure, Short Sale, and Judgments

Many people believe that a foreclosure, bankruptcy, short sale, or judgment means they will never…

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

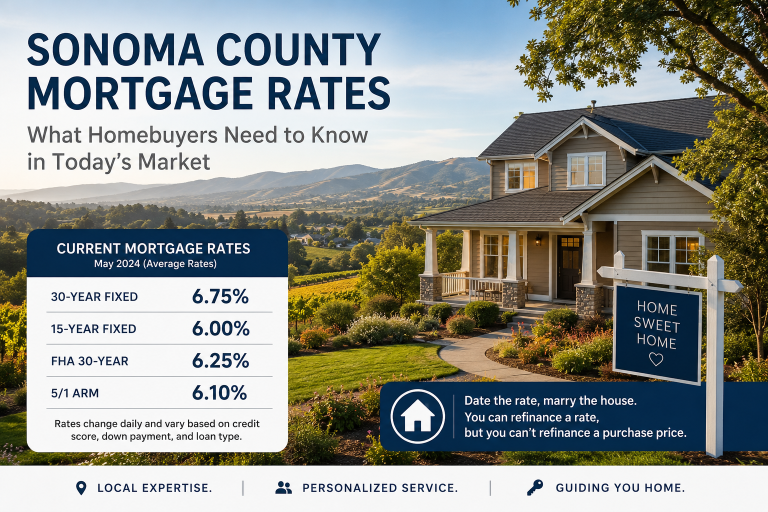

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!