Everyone dreams of buying a home at just the right moment—when prices are low, rates are perfect, and the competition has cooled off. The reality? Perfect timing in real estate is nearly impossible. What you can do is focus on the practical factors that tell you when it’s the right time for you to buy, not when the headlines say it is.

The Myth of Perfect Timing

Many would-be buyers wait for the “ideal” rate or price, but the market rarely moves in perfect harmony with personal circumstances. Rates fluctuate daily, home prices shift by neighborhood, and waiting too long can mean paying more later—especially if home values keep rising or rents increase faster than your ability to save.

The truth is, most successful homeowners didn’t buy at the perfect time—they bought when it made financial sense for their lifestyle and budget.

1. Focus on Affordability, Not Headlines

Trying to predict the housing market is like trying to predict the stock market. Instead of chasing the lowest interest rate, look at your monthly payment comfort zone. Can you afford the mortgage, taxes, insurance, and maintenance without stretching yourself thin? That’s the metric that matters most.

Your lender can help you model payments at different price points and rate scenarios. If the payment works within your budget and goals, it may already be the “right” time to buy. For help understanding how affordability changes with rates, read

How Much Home Can You Really Afford?

2. Evaluate Your Financial Readiness

Ask yourself: Are your finances stable? Do you have steady income, manageable debt, and enough cash reserves for both a down payment and unexpected expenses? These are the true indicators of readiness—not market timing.

Being prepared means having an emergency fund and a cushion beyond closing. It’s better to buy in a slightly higher-rate environment with strong reserves than to rush into a low-rate purchase that leaves you cash-poor. Learn more in

The Smart Way to Use Your Home Equity.

3. Consider Market Trends—But Don’t Be Ruled by Them

Local trends matter more than national ones. Even when rates rise, supply and demand in your specific area might still create opportunities. For instance, in some Sonoma County neighborhoods, seasonal slowdowns between fall and early spring can bring better negotiating power, even when rates are slightly higher.

Mortgage rates are cyclical. What’s high today can come down tomorrow, which means you can always refinance later if it benefits you. The key is getting into the home that fits your life—not waiting endlessly for the market to match your ideal conditions.

4. Factor in the Cost of Waiting

Delaying a purchase can cost more than you think. While waiting for rates to drop half a percent, home values could increase 5%—or more—offsetting any rate savings. Meanwhile, you’ve missed months (or years) of potential appreciation and principal reduction that build wealth over time.

The cost of waiting is especially real in strong markets where demand outpaces inventory. Acting when you’re ready means starting your wealth-building journey sooner, even if conditions aren’t “perfect.”

5. Match Your Mortgage to Your Timeline

Choose a loan program that matches how long you plan to stay in the home. A fixed-rate mortgage offers predictability if you’ll stay long-term, while an adjustable-rate loan could save money if you expect to sell or refinance in a few years. The right mortgage strategy should align with your personal goals—not market speculation.

Bottom Line: The Right Time Is Personal

Buying a home isn’t about timing the market—it’s about timing your life. If you have the financial stability, job security, and personal readiness to take on homeownership, that’s your best moment to buy. The market may never feel “perfect,” but owning a home that fits your life can be the smartest long-term move you’ll ever make.

Looking to get a mortgage? Get a complimentary mortgage rate quote now.

Share:

RELATED MORTGAGE ADVICE FROM SCOTT SHELDON

Why Lower Mortgage Rates May Require More Income to Buy a Home in Sonoma County

When mortgage rates fall, most people immediately assume buying a home becomes easier. At first…

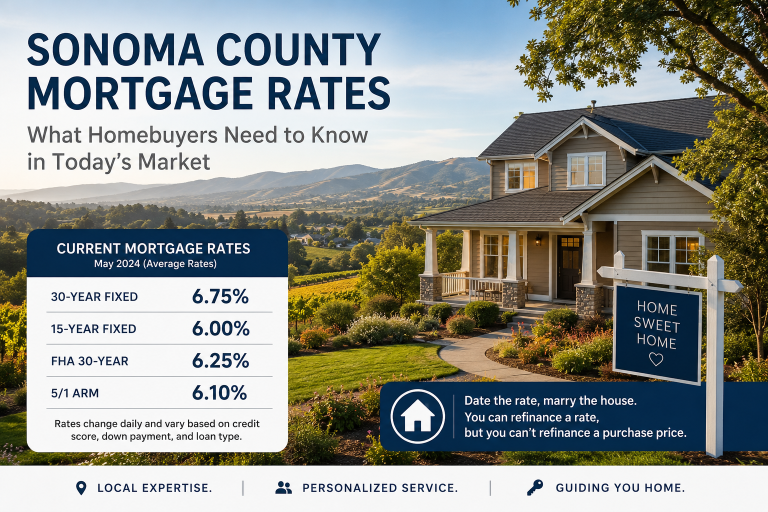

What Homebuyers Need to Know in Today’s Market

If you’ve been thinking about buying a home in Sonoma County, you’re probably paying close…

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping Their Current Home

Can You Have Two FHA Loans at Once? What Homebuyers Need to Know Before Keeping…

Manufactured Homes: Why the June 15, 1976 Build Date Matters More Than You Think

If you are thinking about buying a manufactured home, one of the most important details…

View More from The Mortgage Files:

begin your mortgage journey with sonoma county mortgages

Let us make your mortgage experience easy. Trust our expertise to get you your best mortgage rate. Click below to start turning your home dreams into reality today!