Let’s start with a simple scenario. You’re looking at two homes. One is fully updated, clean, and ready to go—but it comes with a higher price and higher monthly payment. The other needs some work—maybe paint, flooring, or a few updates—but it’s priced lower. Which one is the better investment? From experience as a landlord,…

Let’s start with a simple idea: trying to perfectly time the housing market is not a winning strategy. It sounds good in theory. Wait for rates to drop. Wait for prices to fall. Wait for the “right moment.” But here’s the reality—no one consistently gets that timing right. Not individual buyers. Not seasoned investors. Not…

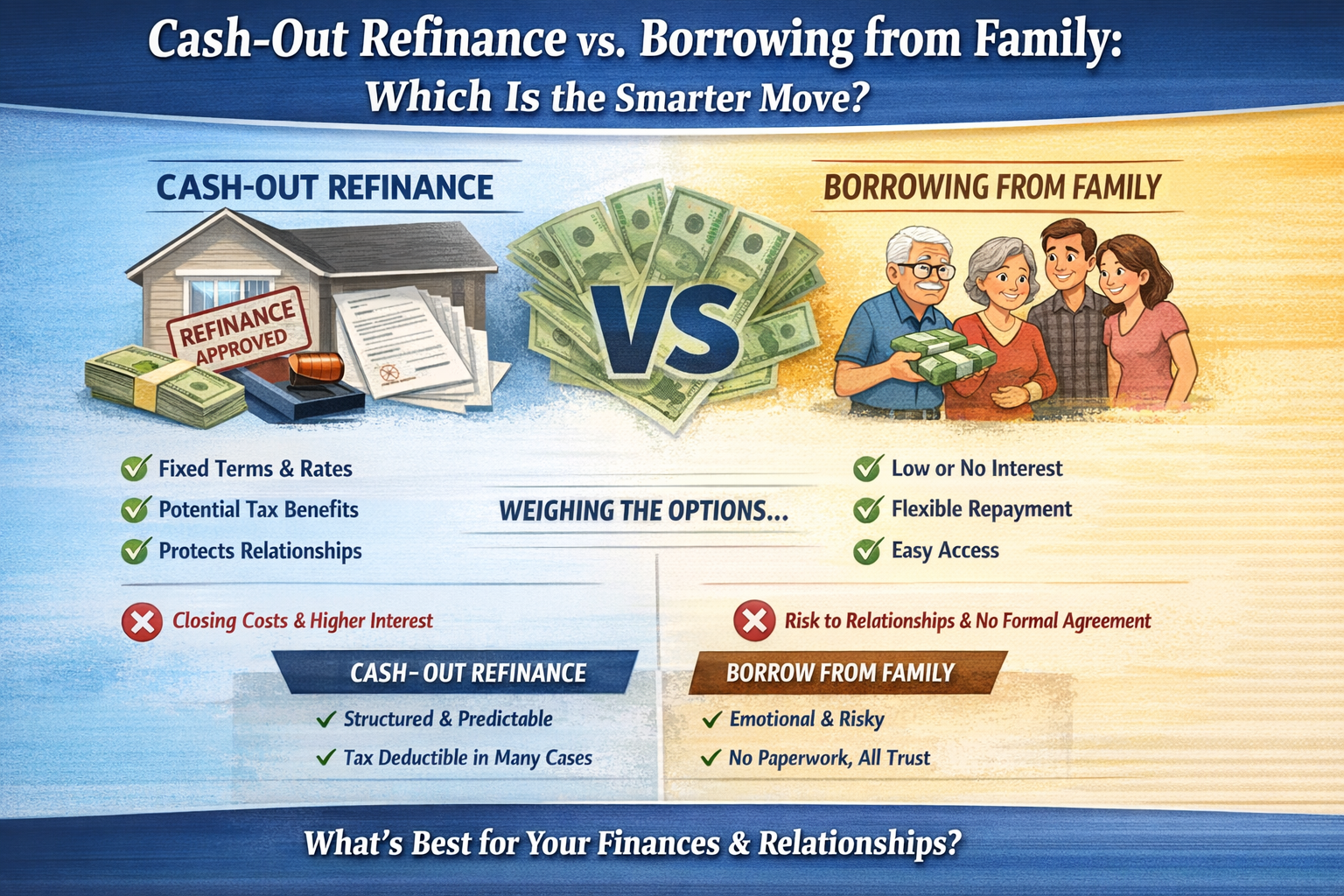

You’ve built equity in your home. Maybe a lot of it. At the same time, you need access to cash—whether that’s to consolidate debt, invest in real estate, fund a business, or handle a life event. Now you’re standing at a fork in the road: Do you tap into your home equity with a cash-out…

Who you use for a mortgage loan matters. Let’s walk through a very real scenario that happens all the time when someone is considering refinancing their home. Imagine you currently have a 6.25% conventional mortgage. You’re looking at refinancing because you see interest rates drifting lower. You call a lender and they quote you 5.25%.…

For many buyers, the idea of buying a vacant parcel of land and building their dream home—or placing a manufactured home on it—sounds both exciting and affordable. On paper, it may even look cheaper than buying a resale property in today’s competitive housing market. But the reality? Building from scratch, especially on raw land, or…

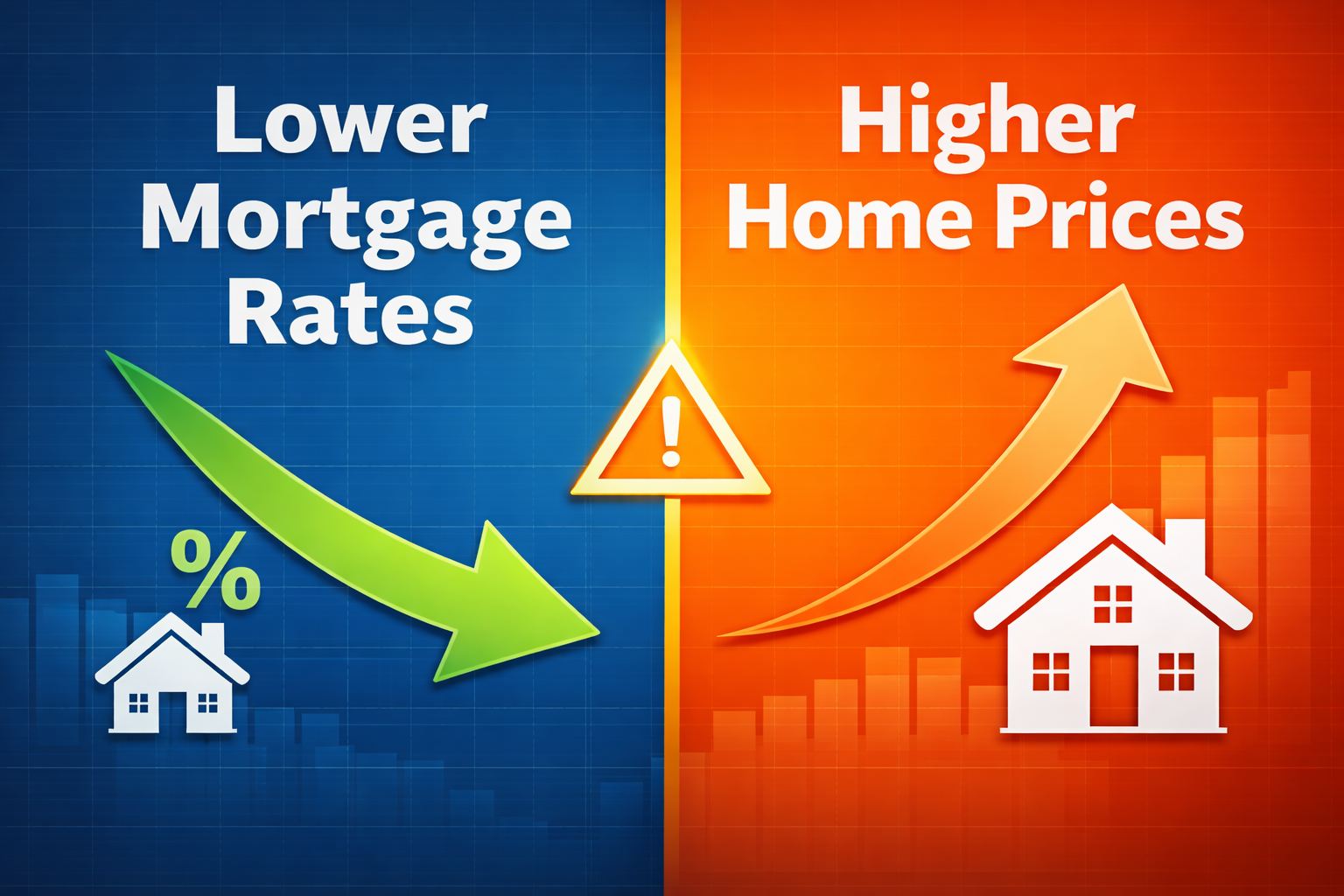

Everyone loves the idea of lower mortgage rates—and for good reason. A lower rate means a lower monthly payment and more buying power. But here’s the part that often gets overlooked: when mortgage rates fall, home prices often rise. And sometimes, those rising prices can cancel out the benefit of a lower rate. This creates…

Let’s face it—everyone wants to know when mortgage rates will drop. Whether you’re buying your first home, refinancing an existing loan, or just watching from the sidelines, it’s tempting to wait for the “perfect” rate. But here’s the truth: no one can predict how low mortgage rates will go, not even the experts. That’s because…

Over the past week, there has been a lot of noise around mortgage rates. Headlines moved fast, social media lit up, and many buyers and homeowners were left wondering the same thing: “Are rates finally coming down?” The short answer, as of mid-January, is no. Mortgage rates are essentially unchanged. Last week, President Trump made…